(FWA 2026/5/29)The number of New Immigrants and foreign spouses in Taiwan is nearly 620,000, making them core members of many industries and families, with an increasing demand for financial services and wealth management. The TransAsia Sisters Association, Taiwan (TASAT) and Taipei Fubon Bank released the “New Immigrants Financial Needs Survey” on the 29th. The survey revealed that 70% of respondents have a high demand for financial services, and half hope to improve their financial knowledge, but they still face barriers. To stay close to actual life contexts, the survey first conducted focus groups, followed by a questionnaire in seven languages—Vietnamese, Indonesian, Thai, Philippine, Burmese, Cambodian, and Chinese—collecting a total of 490 valid responses. To turn the survey into practical support, both parties are jointly promoting New Immigrants financial empowerment courses and a seed teacher program to enhance New Immigrants’ understanding and application of financial knowledge and services.

Over 40% of Respondents Experienced Multiple Document Submissions

TASAT Secretary-General Chen Hsueh-hui explained that the survey found over 70% of New Immigrants are the primary managers of their household finances, possessing a continuous and independent need for financial services. However, when actually handling financial transactions, respondents still face three major barriers: operational anxiety, digital risks, and unclear procedures.

Although some respondents have daily language communication skills, they still have difficulty understanding specialized financial terminology and non-routine information. The barrier is not just language, but information comprehension and unclear procedures. 23.1% of respondents cannot read Chinese or instructions, feel stressed because they do not know what documents to prepare (21.4%), and an even higher percentage feel pressured when asked to explain the purpose of their transactions (17.6%).

Digital Finance Operational Anxiety and Fear of Transferring to the Wrong Account

Digital financial services have gradually become widespread. Among the respondents, 37.3% use digital apps and 31.6% use ATMs. However, they feel uneasy about digital financial operations (21.2%), worrying most about pressing the wrong button or transferring to the wrong account (48.8%), personal data leaks (44.3%), being scammed (43.5%), or having their accounts locked (28.6%).

The lack of transparency in financial service processes and the uncertainty caused by application experiences also create actual barriers. 29.0% of respondents have been afraid to go to a bank/post office or have delayed doing so (relying on family assistance) because they do not know the process or are afraid of being asked too many questions; over 40% of respondents have had to visit the bank multiple times and submit supplementary documents for a single financial procedure; 31.6% have been rejected or repeatedly asked for reasons when opening an account, applying for a card, or opening an investment account.

TASAT Chairperson Hung Man-chih shared that although she possesses a certain level of literacy, when she first started handling over-the-counter financial services, she often made filling errors and even had to practice at home beforehand. Using digital apps also frequently required her to go to the counter to unlock her account due to input errors. She once failed a digital remittance due to unfamiliarity with the procedure and, in a panic, asked a friend to remit the money on her behalf.

Wu Yi-ting, a second-generation New Immigrant who participated in the initial focus group, shared that her mother was very afraid of going to the bank because she was unfamiliar with Chinese characters. When helping her mother open an account, the application was initially rejected, and her mother would likely struggle to handle the complex details on her own. She also once accompanied her mother step-by-step to help her memorize the ATM operation process, which attracted the attention of bank security who repeatedly confirmed their relationship, making the mother and daughter feel as if they were suspected of being money mules. The survey also found that nearly a quarter of respondents had encountered fraud (23.9%), and those who self-assessed their Chinese proficiency as better actually had a higher rate of being scammed, possibly because they are more easily exposed to fraudulent situations.

Nearly 30% Afraid to Enter Banks, Relying on Relatives and Children

In addition to the difficulties encountered in usage, the survey also shows that New Immigrants’ need for financial education gradually extends to old age and family financial arrangements. This also reflects that many marriage immigrants who came to Taiwan have entered middle and old age (those aged 41-65 account for about 60% of the respondents). 56.1% of respondents want to learn financial knowledge about saving money and retirement preparation, 36.7% about fraud prevention and account protection, and over 30% want to learn about basic investing, medical care, and long-term care protection.

Regarding learning methods, half of the respondents can accept all-Chinese instruction but hope for fewer specialized terms and more practical case studies (48.6%), situational practice through methods like practicing transfers and verification (46.7%), and the use of their native language paired with Chinese keywords.

Hsia Hsiao-chuan, a professor at the Graduate Institute of Social Work at National Chengchi University, pointed out that the issues faced by many New Immigrants entering middle and old age are no longer the adaptation problems of when they first arrived, but rather issues of security in old age. Whether they can use financial services equally is closely related to whether they can age with peace of mind. She called on financial institutions to think from the concept of New Immigrants’ financial equity—not just providing additional services that can be understood and used, but incorporating their experiences and needs into the design, expanding financial equity under the premise of ensuring financial security.

Turning the Report into Action: Recruiting Seed Teachers for New Immigrant Financial Courses

Yang Ya-yuan, Senior Assistant General Manager of the Brand Sustainability Department at Taipei Fubon Bank, expressed her agreement. She believes that equity means allowing people to accomplish what they want without needing extra assistance. The first thing Taipei Fubon Bank can do is break down the language barrier on the front lines or online, providing bilingual process materials in native languages to eliminate insecurity.

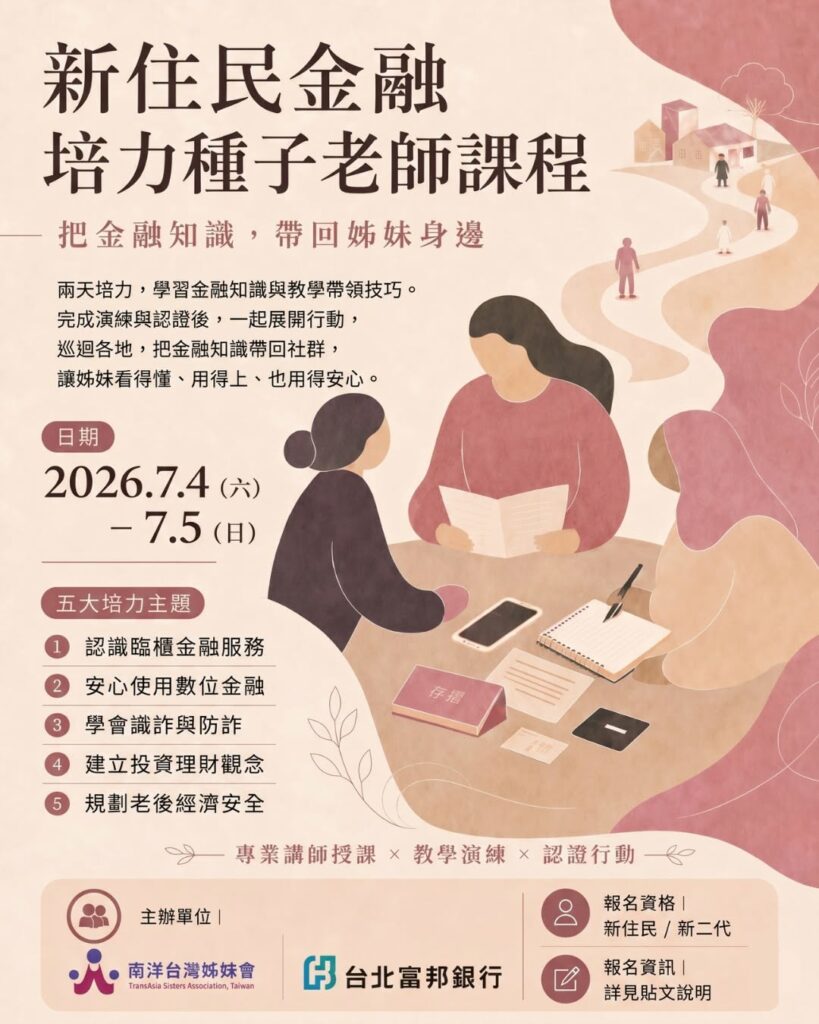

New Immigrants are not bystanders to financial services, but the people who actually handle household financial affairs every day. To this end, TASAT and Taipei Fubon Bank have officially launched actions following the release of the survey report, cooperating to organize the “New Immigrants Financial Empowerment Seed Teacher Course,” which will deepen empowerment in over-the-counter handling, digital operations, fraud prevention, wealth management, and old-age economic security.

The project expects to recruit 10 to 12 New Immigrants and second-generation New Immigrant partners. During the two-day course, professional instructors will guide them in learning financial knowledge and teaching leadership skills. Through practice and certification, trainees will become seed teachers who can go into the community to share and deeply promote financial education on tour in various places.

[Course and Registration Information]

Eligibility: New Immigrants / Second-generation New Immigrants

Course Dates: July 4, 2026 (Sat) to July 5, 2026 (Sun)

Course Location: Taipei City (to be notified separately)

Five Core Themes:

Understanding over-the-counter financial services

Using digital finance safely

Learning to recognize and prevent fraud

Establishing investment and wealth management concepts

Planning for old-age economic security

Online Registration URL: https://reurl.cc/N2KmEp

{kind=link}